4th Klagenfurt-Bielefeld Summer School on Modern Topics in Time Series Analysis 2024

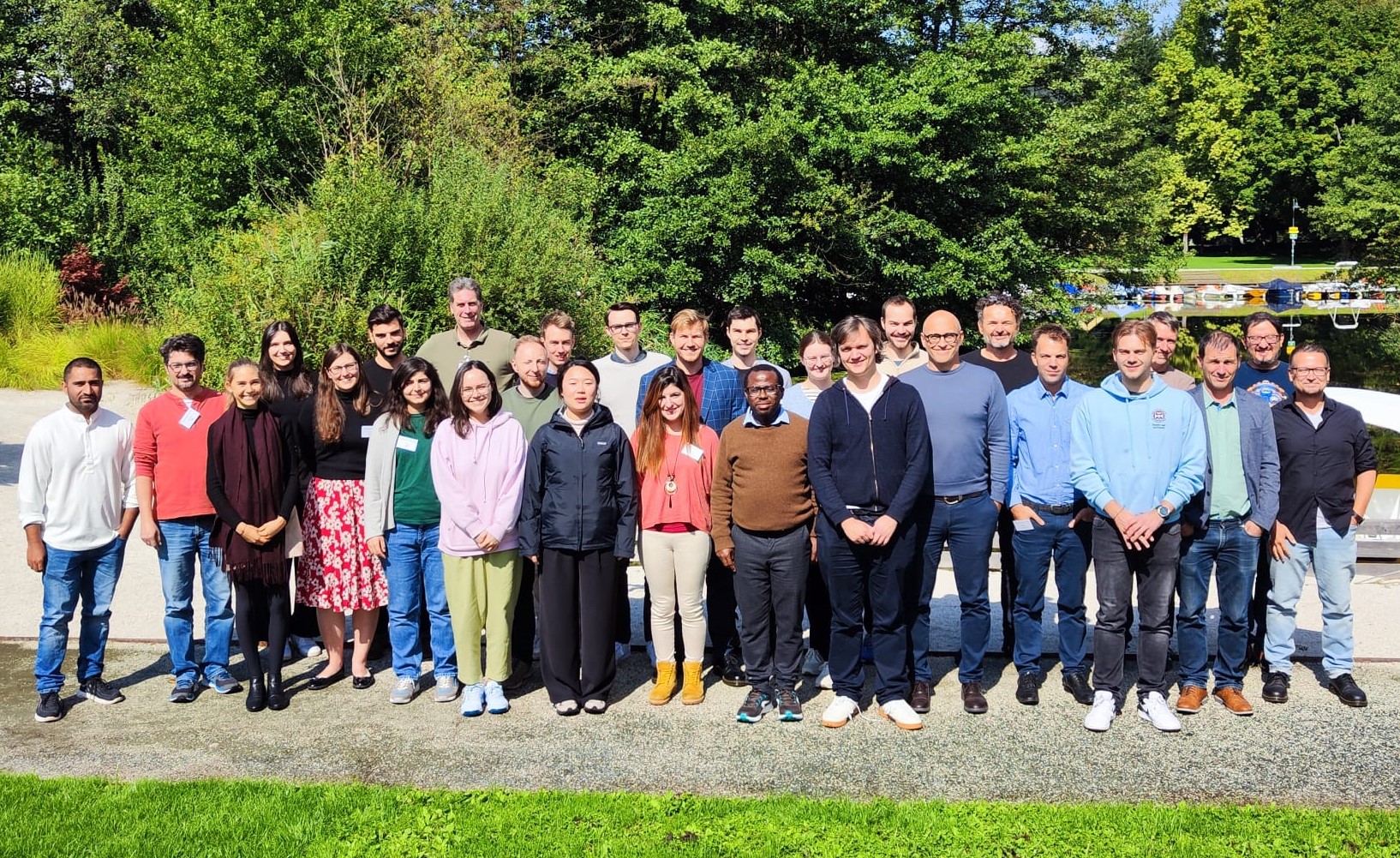

In the week of September 16, 2024, twenty-six junior researchers (twenty predocs and six postdocs) from nineteen universities, companies and banks from ten countries convened in Klagenfurt for an entire week to extend their skills in modern topics in time series analysis. International experts in the fields of econometrics and statistics presented a wide body of knowledge in sixteen lectures, ranging from introductory subjects to the newest findings in top-level scientific research. This included detailed coverage of factor models, state-space modelling, Bayesian methods, functional time series models, models for non-linear cointegration, modelling of climate channge, Hidden Markov models, robust inference and forecasting of time series with seasonalities and trends.

Organizer Prof. Dr. Martin Wagner: „Modern topics in time series analysis increasingly determine everyday life of companies, public institutions and research establishments. It is, therefore, elementary for young graduates not only in statistics and econometrics but also – increasingly and more frequently demanded – in business and economics to be familiar with such methods and able to use them sensibly. Keeping this in mind, the summer school provides the participants with concise insights into a large number of interesting topics. The highly positive reactions confirm that the lectures not only provide PhD students with valuable insights but also that practitioners can take many suggestions with them and look forward to applying them in practice.

The participants’ feedback was positive throughout, not only with regard to contents and the excellent lecturers but also the organization and the setting which provides a balanced mix of lectures and breaks, allowing for ample exchange with the lecturers and other participants and plenty opportunities to establish new contacts.

„As a participant, I found this workshop highly beneficial and interesting as it covers a wide range of time series concepts that are essential for PhD students, practitioners, and Master’s students. The lectures provided valuable materials and encouraged open discussions. The diversity within the group of participants from different universities and backgrounds made the exchange of ideas and perspectives particularly productive” says Alexandros Konstantopoulos, PhD student at the Quantitative Economics Division.

Topics and Lecturers:

- Seasonal and Trend Modelling: Forecasting von Harry Haupt (University of Passau)

- Hidden Markov Models: Timo Adam (Bielefeld University)

- Nonlinear Cointegration: James Duffy (Oxford University)

- Bayesian Methods for (Macro and Financial) Time Series Analysis: Gregor Kastner (University of Klagenfurt)

- State Space Modelling: Dietmar Bauer (Bielefeld University)

- Functional Time Series Analysis: Hörmann Siegfried (Graz University of Technology)

- Econometric Modelling of Climate Change: Eric Hillebrand (University Aarhus)

- Dynamic Factor Models: Manfred Deistler (Vienna University of Technology)

- Robust Inference for the Long Run: Martin Wagner (University of Klagenfurt)

Organization: Prof. Dr. M. Wagner (University of Klagenfurt), Prof. Dr. D. Bauer (Bielefeld University)

Financial support was granted by the Research Council of the University of Klagenfurt and Verein zur Förderung der Wirtschafts- und Rechtswissenschaften an der Universität Klagenfurt.